Beauty Tools & Accessories

The Bottom 50%

Jun

The Bottom 50% sounds like a gloomy scoreboard, the kind nobody wants to see next to their name. But in economics, the phrase is not an insult, a horoscope, or a motivational poster gone wrong. It usually refers to the lower half of households by wealth, income, or financial security. In the United States, that group includes millions of working people, families, retirees, students, caregivers, renters, small-business strivers, and folks who can stretch a dollar so far it deserves Olympic recognition.

Understanding the bottom 50% matters because it tells us how the economy feels from the checkout line, the rent portal, the repair shop, and the kitchen table. Stock indexes may rise, GDP may grow, and corporate earnings may sparkle like a freshly waxed sports car, but if half of households still have little room for emergencies, savings, homeownership, or retirement, the story is incomplete. The economy is not just a chart. It is whether the car starts, whether the fridge stays full, and whether a $400 surprise expense becomes a small inconvenience or a three-act drama.

What Does “The Bottom 50%” Mean?

The bottom 50% typically means the lower half of households ranked by net worth. Net worth is simple in theory: assets minus debts. Assets include checking accounts, savings, homes, retirement accounts, vehicles, investments, and businesses. Debts include mortgages, credit cards, student loans, auto loans, medical debt, and personal loans. In real life, calculating net worth can feel like opening a junk drawer full of receipts, but the formula is still straightforward.

When economists discuss the bottom 50%, they are not saying every household in that group is poor. Some may own a modest home, have a pension, or hold savings. Others may have negative net worth because debt outweighs assets. The category is broad, which is exactly why it is useful. It shows how much national wealth is held by the half of households with the least wealth and how far that group sits from the middle, the top 10%, and the top 1%.

Income Is Not the Same as Wealth

Income is what flows in: wages, salary, tips, benefits, business earnings, Social Security, interest, and other payments. Wealth is what remains after years of earning, spending, saving, investing, borrowing, and paying down debt. A household can have decent income and low wealth if expenses are high, debts are heavy, or emergencies keep draining savings. Another household can have modest income but meaningful wealth because it owns a paid-off home or has retirement assets.

This distinction matters because the bottom 50% is often squeezed from both sides. Many households do not earn enough to save consistently, and without savings, they miss the engine that grows wealth: compound returns, home equity, retirement contributions, and emergency buffers. In other words, income pays the bills; wealth buys breathing room.

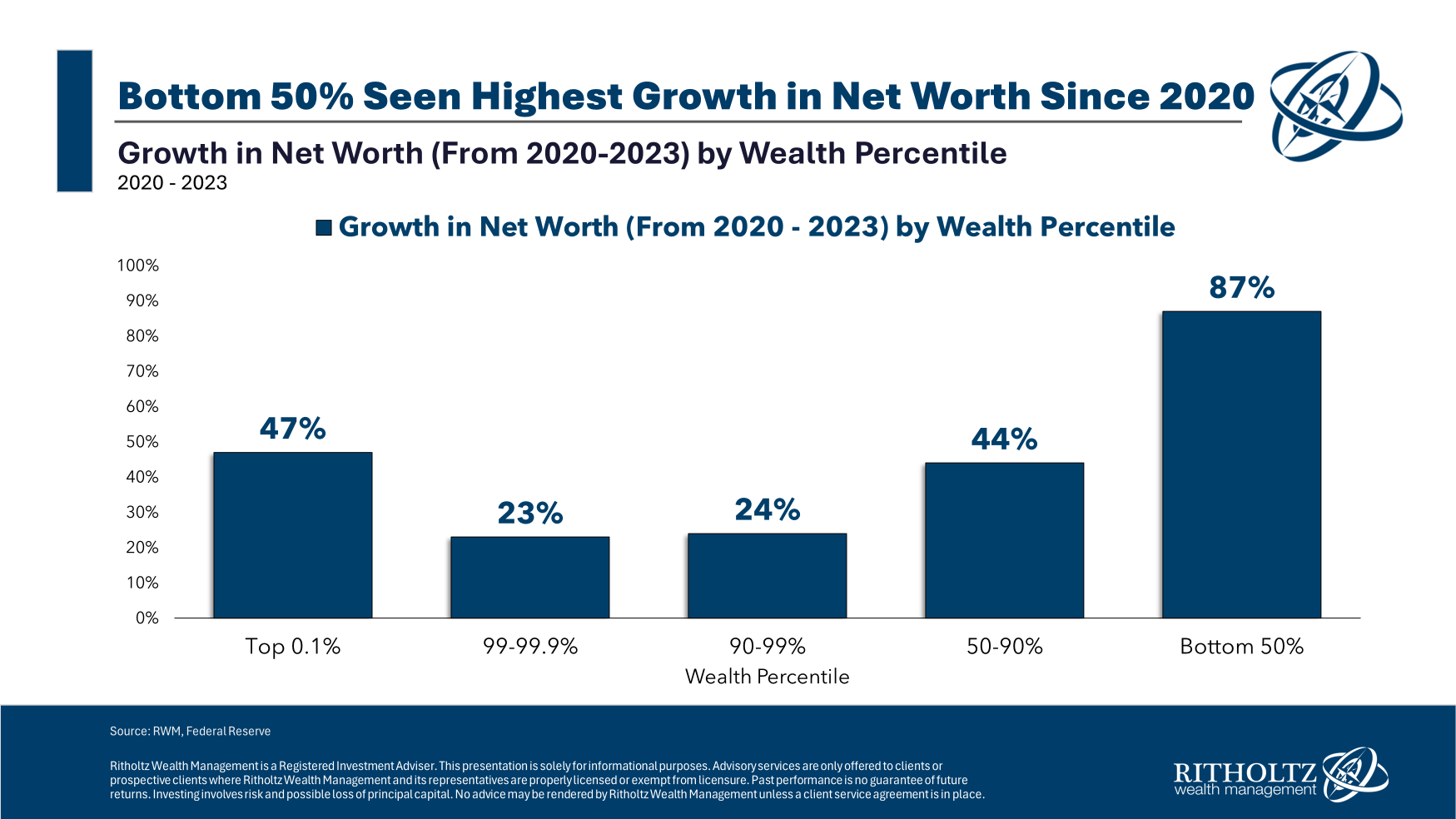

The Big Picture: Why the Bottom Half Owns So Little

Recent U.S. data shows a striking gap: the bottom half of households holds only a small share of total household wealth, while the top tiers hold most assets. This is not because the bottom 50% forgot to clip coupons with sufficient enthusiasm. The pattern reflects decades of wage pressure, rising housing costs, uneven access to stock ownership, student debt, medical expenses, childcare costs, and differences in inherited wealth.

The top of the wealth distribution owns a large share of stocks, business equity, investment real estate, and retirement assets. These assets often grow faster than wages. Meanwhile, many bottom-half households depend primarily on labor income. When prices rise faster than paychecks, there is little left to invest. When rent takes a large bite, savings become a rumor. When debt carries high interest, progress can feel like running on a treadmill that charges a monthly fee.

Homeownership: The Classic Wealth Builder With a Taller Fence

For many American families, homeownership has historically been the main path to building wealth. A mortgage payment can become equity; rent usually becomes a receipt and a polite email from the landlord. But home prices, mortgage rates, insurance, property taxes, and maintenance costs have made the front door harder to reach. The down payment alone can feel like a dragon guarding the castle.

Renters face their own pressure. Millions of renter households spend more than 30% of income on housing, and many spend more than half. Once housing takes that much, the budget has to perform circus tricks. Food, transportation, healthcare, childcare, utilities, and debt payments all compete for what remains. Saving for a down payment under those conditions is possible for some, but for many it feels like trying to fill a swimming pool with a teaspoon.

Stocks and Retirement Accounts: A Wealth Rocket Many Miss

The stock market has been one of the most powerful wealth-building tools in modern America. The catch is that people must own stocks to benefit from stock gains. Higher-income households are much more likely to hold substantial investments through brokerage accounts, retirement plans, employer stock, and business ownership. Many bottom-half households either do not have access to employer retirement plans or cannot afford to contribute much after basic expenses.

This creates a quiet but powerful divide. When markets rise, households with investments see their balance sheets grow while households without investments mainly see headlines. It is hard to cheer for a bull market when your financial portfolio consists of a debit card, a tire with a slow leak, and a grocery list written like a hostage negotiation.

Work Is Not MissingFinancial Cushion Is

A common misconception is that the bottom 50% is mostly disconnected from work. In reality, many households in the lower half work hard. The issue is not effort; it is the relationship between effort, pay, costs, and security. Low-wage and middle-wage workers often carry the economy through service jobs, care work, food production, logistics, retail, construction, hospitality, education support, and other essential roles. These jobs keep daily life moving. Unfortunately, many do not produce enough surplus income to build wealth quickly.

Recent wage gains helped many lower-paid workers, especially during tight labor markets. But affordability remains a stubborn opponent. A raise can be real and still be swallowed by rent, groceries, car repairs, insurance premiums, and interest rates. That is the cruel magic trick of modern budgeting: money appears, then vanishes before anyone gets to clap.

The Emergency Expense Test

One of the clearest ways to understand financial fragility is the emergency expense question: could a household cover a sudden $400 bill using cash, savings, or a credit card paid off immediately? Many adults can, but a large share cannot do so comfortably. For bottom-half households, a medical copay, broken alternator, dental bill, or utility spike can become a chain reaction.

Financial instability is rarely one dramatic event. More often, it is a sequence: one missed shift, one late fee, one overdraft, one credit card balance, one delayed car repair, one higher insurance bill. Each piece may look manageable alone. Together, they become the budget version of being pecked by ducks. Not deadly at first glance, but deeply unpleasant and surprisingly persistent.

Debt: Helpful Tool or Financial Trap?

Debt is not automatically bad. A mortgage can help a family buy a home. Student loans can finance education. A credit card can smooth timing between paychecks or protect against fraud. But debt becomes dangerous when it is used to cover basic necessities without enough income to repay it quickly. High-interest credit card debt is especially unforgiving. It grows while people sleep, which is rude behavior for a financial product.

For the bottom 50%, debt often plays two roles at once. It is a bridge and a burden. It helps cover emergencies, transportation, school, or healthcare, but it also drains future income through interest payments. When wages are tight, debt repayment competes with saving. The result is a cycle where households pay for the past while trying to afford the present and somehow plan for the future. That is not a budget; that is a three-ring circus.

Why the Bottom 50% Matters to the Whole Economy

The financial health of the bottom half is not a niche concern. It affects consumer spending, labor market stability, public health, education outcomes, housing demand, small-business revenue, and even political trust. When half of households have limited wealth, the economy becomes more vulnerable to shocks. A downturn, inflation spike, medical crisis, or credit crunch can quickly reduce spending and increase hardship.

Businesses also depend on broad purchasing power. A luxury economy can thrive for a while on high-end spending, but local restaurants, repair shops, childcare providers, grocery stores, barbers, laundromats, and small retailers need regular customers with money left after essentials. The bottom 50% is not just a statistic. It is the customer base, the workforce, the neighborhood, and the future tax base.

Economic Mobility: The American Dream Needs a Tune-Up

Economic mobility means people can move up over time through education, work, entrepreneurship, saving, and opportunity. The United States has long celebrated mobility as part of its national identity. But mobility depends on more than motivation. It depends on affordable housing, quality schools, safe neighborhoods, accessible healthcare, transportation, broadband, childcare, fair lending, and jobs that pay enough to save.

When families lack wealth, they have fewer backup options. A wealthier parent may help with tuition, a down payment, a used car, unpaid internship costs, or a temporary move during a job search. A low-wealth family may offer love, wisdom, and excellent leftoversbut not a $20,000 down payment. That difference compounds across generations.

What Helps the Bottom 50% Build Wealth?

No single policy or personal habit will solve wealth inequality by itself. The bottom 50% is too diverse, and the causes are too layered. But several strategies consistently matter: higher and steadier wages, affordable housing, access to banking, lower-cost credit, retirement plan coverage, debt relief where appropriate, stronger worker bargaining power, childcare support, education and training pathways, healthcare affordability, and tax credits that reach working families.

On the personal finance side, households benefit from emergency savings, automatic transfers, employer retirement matches, high-interest debt reduction, credit score protection, and skill-building that increases earnings. But advice must be realistic. Telling someone to “just invest more” when rent eats half the paycheck is like telling a fish to “just buy hiking boots.” The math has to work.

Small Wealth Is Still Wealth

One of the most important ideas is that small savings can be powerful. A few hundred dollars can prevent an overdraft. A few thousand can stop a car repair from becoming a job loss. A retirement account with modest monthly contributions can become meaningful over decades. A starter emergency fund may not look glamorous, but glamour is overrated when the water heater explodes.

Wealth-building for the bottom 50% does not always begin with investing in the stock market. Sometimes it begins with stability: predictable hours, fewer fees, reliable transportation, affordable rent, and enough savings to avoid expensive borrowing. Stability is the runway. Wealth is the takeoff.

Common Myths About the Bottom 50%

Myth 1: The Bottom 50% Does Not Work Hard

Many households in the bottom half work full time, multiple jobs, irregular schedules, or unpaid caregiving roles. Hard work is common. What is less common is enough surplus income to build assets after necessary expenses.

Myth 2: Budgeting Alone Can Fix Everything

Budgeting helps, but it cannot magically lower rent, erase medical bills, or turn a $15 wage into a $35 housing wage. Personal finance matters, but structural costs matter too. A budget is a map; it is not a teleportation device.

Myth 3: Everyone Benefits Equally When the Economy Grows

Growth helps, but the benefits depend on who owns appreciating assets, who gets wage increases, and who faces rising costs. If asset owners gain faster than wage earners, wealth concentration can increase even during expansion.

Experiences Related to “The Bottom 50%”

To understand the bottom 50%, imagine a household that looks stable from the outside. The adults work. The kids go to school. The car is old but loyal, like a golden retriever with 180,000 miles. Bills are paid most months. There may even be a small savings account. Then the car needs a transmission repair. Suddenly, the household faces a choice: pay the mechanic, delay rent, use a credit card, borrow from relatives, or risk losing transportation to work. Nothing about this situation suggests laziness. It is simply what happens when income is steady but thin and savings are shallow.

Another common experience is the “almost there” problem. A worker gets a raise, but the rent renews higher. A family pays off one credit card, then a medical bill arrives. A young adult starts saving, then student loan payments resume. A parent picks up extra shifts, then childcare costs rise. Progress happens, but it keeps getting interrupted. The bottom 50% often lives in this space: not always in crisis, but always close enough to crisis that peace of mind feels expensive.

There is also a psychological cost. People with little financial cushion spend more mental energy planning around scarcity. They compare gas prices, delay dental care, check bank balances before buying groceries, and calculate whether a school field trip fee fits the week’s budget. This kind of constant decision-making is exhausting. It is not because people are bad with money. It is because every dollar already has a job, and sometimes three dollars show up wearing the same uniform.

At the same time, the bottom 50% is full of creativity. Families share childcare. Neighbors exchange tools. People repair instead of replace. They cook in bulk, hunt for deals, use community programs, work side gigs, and learn financial skills through experience rather than seminars. There is resilience here, but resilience should not be romanticized. Being resourceful is admirable; needing to be resourceful every single day is tiring.

One of the most hopeful experiences is the moment a household gains its first real cushion. Maybe it is $500 in savings. Maybe it is a paid-off credit card. Maybe it is an employer retirement match finally activated. Maybe it is a reliable used car bought without predatory financing. These wins may look small on a national balance sheet, but inside a household they are huge. They change how people sleep. They change how people plan. They turn emergencies back into problems instead of disasters.

For policymakers, business leaders, and communities, the lesson is clear: the bottom 50% does not need pity. It needs systems where work leads to stability, stability leads to savings, and savings lead to wealth. For individuals, the lesson is equally practical: build the first layer of protection whenever possible, avoid high-interest traps, use every employer benefit available, and remember that financial progress is still progress even when it looks boring. In personal finance, boring is often beautiful. Nobody writes a rock anthem about automatic savings transfers, but maybe someone should.

Conclusion: The Bottom 50% Is the Economy’s Reality Check

The bottom 50% is not a fringe group. It is half the country. Its financial condition tells us whether prosperity is broad or narrow, whether work is translating into security, and whether the American dream still has enough seats at the table. The data shows that wealth remains highly concentrated, but the story is not hopeless. Wages can rise. Housing can become more affordable. Savings can grow. Retirement access can expand. Debt burdens can be reduced. Opportunity can be rebuilt.

If the economy wants a healthier future, it cannot simply celebrate the top line while ignoring the bottom half. A strong economy should not require millions of households to perform financial acrobatics just to survive the month. The goal is not to make everyone rich overnight. The goal is more practical and more powerful: fewer households one emergency away from trouble, more families able to save, and more people with a fair chance to turn work into wealth.

Note: This article synthesizes public U.S. economic research and data from reputable institutions, including federal statistical agencies, Federal Reserve sources, housing research organizations, labor research groups, and nonpartisan policy institutes. It is written as original, publication-ready SEO content without source-link clutter.