Beauty Unlocked

Underestimate the U.S. Economy at Your Own Risk

Jun

The U.S. economy has a peculiar habit: just when commentators finish writing its obituary, it sits up, asks for coffee, and starts another company.

That does not mean the American economy is indestructible. Inflation can squeeze households, high interest rates can chill investment, federal debt can limit future choices, and an unexpected shock can still knock growth sideways. Yet predictions of imminent economic collapse repeatedly overlook the same underlying strengths: a vast consumer market, adaptable businesses, deep capital markets, abundant natural resources, world-class research institutions, and a culture that treats business failure as an expensive tutorial rather than a permanent exile.

Underestimating the U.S. economy is therefore riskynot because every optimistic forecast will come true, but because pessimists often mistake turbulence for structural decline. The airplane may shake. That does not automatically mean the wings have fallen off.

The U.S. Economy Is Slower Than a Boomand Stronger Than a Eulogy

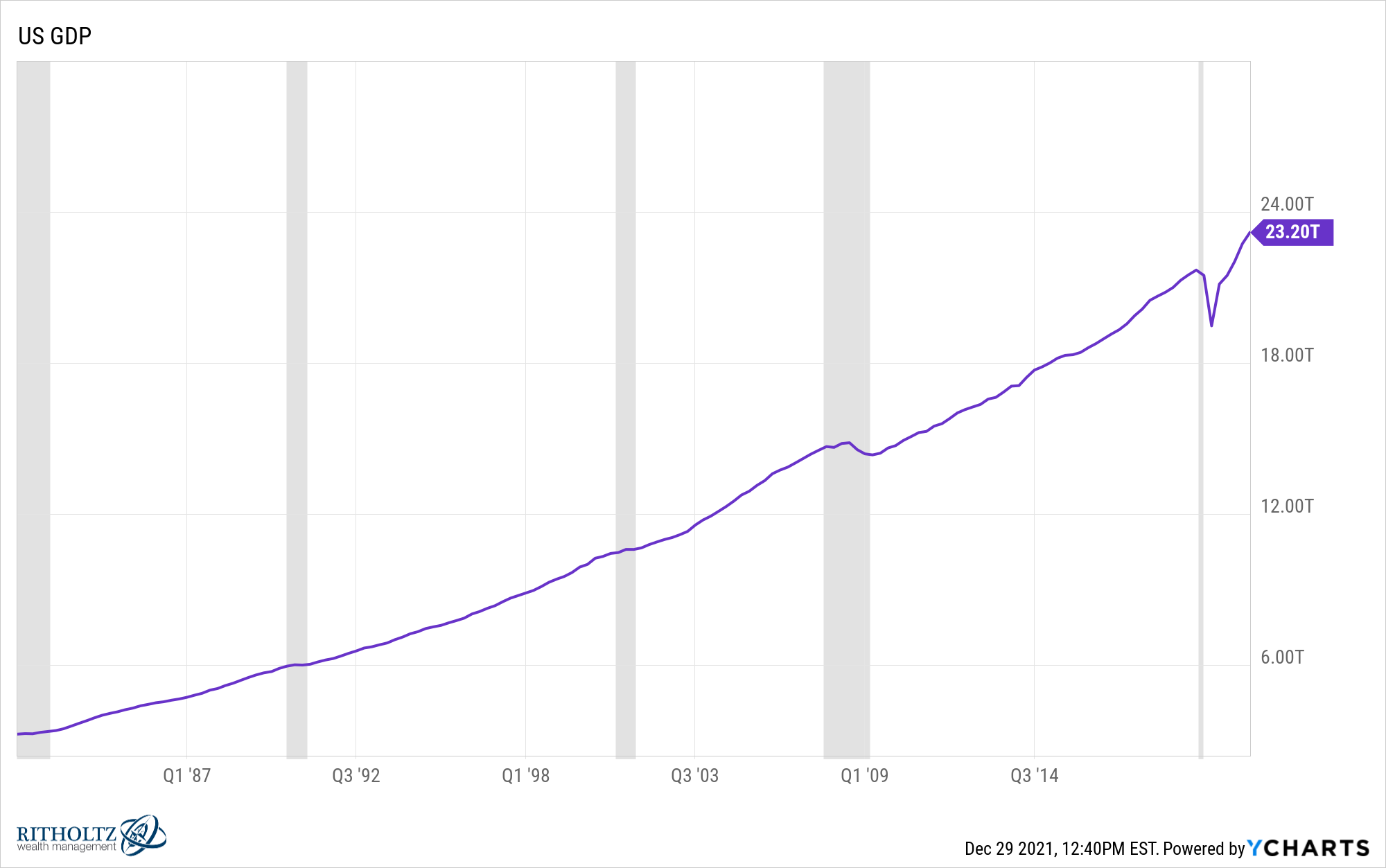

Recent economic data illustrates the problem with dramatic narratives. Real gross domestic product grew at a 1.6% annualized rate in the first quarter of 2026. That was not spectacular, especially after weak growth in the final quarter of 2025, but it was still expansion rather than contraction. Exports, investment, consumer spending, and government spending all contributed.

A moderate quarter is frequently treated as proof that the entire economic engine has stalled. In reality, quarterly GDP is noisy. Imports, inventories, government activity, weather, strikes, tax timing, and business purchasing decisions can all create temporary swings. One quarter is a photograph, not the entire documentary.

Size and diversification create shock absorbers

The American economy is not built around one commodity, one industry, or one coastal financial district. Technology may slow while health care expands. Manufacturing may weaken while construction accelerates. Energy-producing states may benefit from conditions that hurt fuel-intensive businesses elsewhere.

This diversification does not eliminate recessions. It does, however, give economic activity more routes around a blockage. A country that produces software, aircraft, medical devices, financial services, crops, entertainment, pharmaceuticals, industrial machinery, and large quantities of energy has more options than an economy dependent on a single export.

Consumers remain a giant economic force

Consumer spending is one of the central engines of U.S. growth. Hundreds of millions of residents continuously purchase housing, transportation, health care, food, entertainment, education, digital services, and approximately seventeen billion varieties of snack food.

The scale of this internal market allows successful companies to grow substantially without immediately relying on overseas demand. It also gives global companies a compelling reason to invest in American distribution centers, offices, data infrastructure, retail systems, and production capacity.

Consumer strength is not distributed evenly, of course. Higher-income households generally have greater exposure to rising stock and property values, while families with limited savings are more sensitive to rent, food, insurance, and borrowing costs. Still, the national household balance sheet remains enormous. At the end of 2025, household and nonprofit net worth stood at roughly $184.1 trillion.

That wealth provides a formidable cushion, although it must not be confused with universal financial comfort. Aggregate prosperity can coexist with a household wondering why a bag of groceries suddenly requires venture capital.

The Labor Market Keeps Bending Without Easily Breaking

Employment is another reason predictions of immediate collapse require caution. In May 2026, the unemployment rate was 4.3%, remaining within the relatively narrow range seen since mid-2025. Payroll employment increased by about 172,000 during the month.

Those figures do not describe a red-hot labor market. Hiring has become more selective, workers in some industries are experiencing layoffs, and younger professionals face legitimate uncertainty as artificial intelligence changes entry-level tasks. Nevertheless, an unemployment rate slightly above 4% is not evidence of economic free fall.

American workers and companies adapt

The U.S. labor market is unusually dynamic. Workers change employers, move between industries, start businesses, acquire credentials, perform freelance work, and relocate geographically. Companies reorganize quicklysometimes so quickly that employees discover the reorganization through a calendar invitation titled “Quick Catch-Up.”

This flexibility can be painful. Job transitions are rarely as elegant as economists make them sound. A displaced worker cannot pay the mortgage with a chart about long-term productivity. Yet adaptability helps resources move toward growing industries rather than remaining indefinitely trapped in shrinking ones.

Entrepreneurship is an economic renewal system

In May 2026 alone, the Census Bureau recorded more than 523,000 seasonally adjusted business applications. It projected that nearly 29,500 employer businesses would emerge from that month’s applications within four quarters.

Not every application becomes the next household-name corporation. Many will remain tiny, pivot repeatedly, or disappear. That is part of the mechanism. Entrepreneurship involves experimentation at enormous scale: thousands of people testing services, products, technologies, and local business models to discover what customers will actually buy.

The United States has approximately 36.2 million small businesses. Together, they employ nearly 46% of private-sector workers and account for a substantial share of economic activity. This broad base matters. Economic renewal is not limited to famous technology founders wearing identical T-shirts. It also comes from contractors, restaurants, logistics firms, medical practices, manufacturers, retailers, consultants, and software companies solving unglamorous but profitable problems.

Innovation Is the Economy’s Not-So-Secret Weapon

One of the strongest arguments against long-term American economic pessimism is the country’s capacity to convert research, capital, talent, and commercial ambition into new industries.

The United States performed an estimated $940 billion in research and development in 2023. Businesses conducted about 78% of that work, demonstrating that innovation is not confined to government laboratories or university campuses. It is embedded in commercial competition across information technology, biotechnology, chemicals, aerospace, transportation, electronics, medicine, and professional services.

Artificial intelligence may raise productivityand create disruption

Artificial intelligence is already encouraging large investments in data centers, advanced chips, cloud infrastructure, power generation, software, and specialized services. The immediate economic effects are uneven. Some companies are becoming more productive; others have purchased expensive AI tools and are now searching desperately for the problem those tools were supposed to solve.

Over time, however, technologies that reduce the cost of analysis, coding, design, administration, communication, and research could increase output per worker. Even modest improvements in productivity, compounded across a huge economy, can produce significant gains in wages, profits, and living standards.

The transition will also create losers. Certain entry-level responsibilities may disappear, and some occupations will be redesigned faster than training systems can respond. The appropriate conclusion is not that innovation is harmless. It is that the U.S. economy possesses an unusually powerful ecosystem for funding, deploying, and scaling it.

Energy abundance strengthens economic resilience

Technology is only one side of the story. The United States also possesses immense agricultural, mineral, and energy resources. U.S. crude oil production reached a record average of 13.6 million barrels per day in 2025, even though operators used fewer active rigs and drilled fewer wells than in the previous year.

That improvement reflects productivity, engineering, infrastructure, and accumulated expertise. Domestic energy production does not insulate the country from global price shocks, but it improves flexibility, supports exports, attracts energy-intensive industries, and reduces certain external vulnerabilities.

Meanwhile, investments in natural gas, nuclear power, renewables, storage, transmission, and grid technology are expanding the meaning of energy strength. The future advantage will not belong solely to the country with the most fuel. It will belong to the country capable of delivering reliable, affordable power to factories, homes, electric vehicles, and energy-hungry computing infrastructure.

Why the Skeptics Still Have a Case

Respecting the strength of the U.S. economy does not require pretending every warning light is decorative. Several genuine risks could weaken growth or reduce the benefits that ordinary households receive from it.

Federal debt is consuming financial room

The Congressional Budget Office projects that federal debt held by the public could rise from approximately 101% of GDP in 2026 to 120% by 2036. It also expects net interest costs to claim a growing share of national output.

High debt does not automatically cause a crisis. The United States borrows in its own currency, operates deep financial markets, and issues assets used throughout the global financial system. Still, rising interest costs leave less fiscal room for infrastructure, research, defense, social programs, tax relief, or emergency responses.

The risk is less like a cinematic explosion and more like termites in the budget. Nothing appears to collapse today, but future choices become progressively narrower and more expensive.

Household debt and affordability pressures matter

Household debt reached approximately $18.8 trillion in the first quarter of 2026. Most of it consisted of mortgages, and aggregate delinquency measures did not signal widespread collapse. However, borrowers with high credit-card balances, auto loans, student debt, or adjustable financing remain vulnerable.

Housing affordability is especially problematic. High home prices, limited supply in many desirable areas, property taxes, insurance costs, and elevated mortgage rates have made ownership difficult for younger households. An economy can post respectable GDP growth while millions of residents feel locked outside its most important wealth-building mechanism.

Aggregate wealth can hide unequal experiences

National statistics often resemble the average temperature in a hospital: technically measurable, occasionally informative, and not sufficient to determine how each patient is doing.

A booming stock market disproportionately benefits households that own substantial financial assets. A strong national employment report can coexist with layoffs in media, technology, finance, or manufacturing. Rural regions may face different challenges from fast-growing metropolitan areas. Economic resilience is real, but so is the uneven distribution of its rewards.

Trade and policy uncertainty can delay investment

Tariffs, regulatory shifts, immigration changes, tax uncertainty, geopolitical conflict, and supply-chain disruptions complicate long-term planning. Businesses can adapt to many policies. What they dislike most is not always strictness, but unpredictability.

A factory, semiconductor plant, power station, or logistics network requires years of planning. When the rules may change after every election, board meeting, court ruling, or social-media post, companies demand higher returns before committing capital. Persistent uncertainty can reduce investment even when current demand remains healthy.

Economic Resilience Is Not the Same as Economic Invincibility

The most useful way to think about the U.S. economy is neither “unstoppable” nor “doomed.” It is a highly adaptive system with exceptional assets and serious maintenance problems.

Do not confuse a slowdown with a collapse

Growth naturally fluctuates. Higher interest rates are designed to restrain borrowing and demand. Businesses adjust inventories. Consumers postpone major purchases. Housing activity responds to mortgage rates. These processes can produce several disappointing quarters without creating a deep recession.

Investors and business leaders who react to every soft data release as though the economic apocalypse has scheduled a conference call may miss attractive opportunities. During slower periods, labor becomes easier to recruit, commercial leases can become negotiable, competitors retreat, and asset prices sometimes return to reality.

Watch mechanisms, not moods

Consumer confidence surveys and financial headlines can be useful, but economic turning points usually appear through mechanisms: tightening credit, falling employment, declining income, rising delinquencies, reduced capital spending, shrinking orders, and deteriorating business formation.

A gloomy population can continue spending and working. An optimistic population can suddenly discover that banks are no longer lending. Mood matters, but cash flow usually wins the argument.

What the Strength of the American Economy Means in Practice

For business owners, the lesson is to avoid building strategy around either permanent prosperity or permanent disaster. Maintain liquidity, control unnecessary debt, diversify suppliers, and continue investing in capabilities that improve productivity. Defensive preparation and long-term optimism are not opposites. They are roommates who should learn to share the refrigerator.

For workers, adaptability is increasingly valuable. Technical literacy, communication, judgment, relationship management, and the ability to use new tools will matter across industries. The safest career is not necessarily the one untouched by technology. It may be the one in which a worker learns to direct technology better than competitors do.

For investors, resilience argues against making extreme, irreversible bets based on short-term narratives. The U.S. economy has survived wars, financial crises, inflation, political upheaval, technological displacement, energy shocks, and a pandemic. That history does not guarantee future returns, but it should make anyone cautious about betting everything on permanent American decline.

Experience-Based Lessons: What Economic Cycles Teach Us

Practical experience across past economic cycles reveals a recurring pattern: the U.S. economy often looks weakest precisely when adaptation is occurring below the surface.

Lesson one: headlines usually arrive after behavior has changed

By the time a recession, recovery, hiring boom, or inflation wave becomes obvious in national headlines, households and businesses have often been adjusting for months. A restaurant owner sees customers ordering cheaper meals before an economist publishes a consumer-spending analysis. A trucking company notices softer freight volumes before a national report confirms slower goods demand. A recruiter sees fewer job openings before the unemployment rate moves materially.

The same delay applies during recoveries. Companies quietly restore hours, rebuild inventories, approve delayed projects, and contact former customers while public opinion remains gloomy. Anyone waiting for complete certainty usually receives it only after opportunities have become more expensive.

Lesson two: strong companies use downturns as construction seasons

When weaker competitors freeze, disciplined businesses often improve. They renegotiate contracts, automate repetitive work, hire talented people who were unavailable during the boom, refine their products, and strengthen customer relationships.

This does not mean every company should spend aggressively during a slowdown. Cash flow remains oxygen. But businesses that merely hide under the desk may emerge from the downturn with the same weaknesses and a new appreciation for office carpeting.

The most resilient operators separate survival expenses from strategic investments. They reduce spending that produces little value while protecting activities that improve efficiency, quality, distribution, brand trust, or customer retention.

Lesson three: local reality can differ sharply from national data

A national economy growing at a respectable rate may feel recessionary in a town dependent on one employer. Conversely, a region experiencing rapid population growth, factory construction, or energy development may boom while national indicators look mediocre.

Business owners should therefore combine national data with local evidence: customer traffic, regional employment, housing permits, commercial vacancies, supplier lead times, loan conditions, and competitor behavior. GDP is useful, but it will not tell a neighborhood contractor whether homeowners within twenty miles are requesting kitchen renovations.

Lesson four: pessimism sounds intelligent, but compounding rewards participation

Economic pessimism often feels sophisticated because risks are specific and vivid. Debt can be measured. Layoffs can be counted. Failed companies make compelling stories. Gradual improvements in software, logistics, medicine, energy efficiency, and worker skills rarely produce dramatic daily headlines.

Yet those incremental improvements compound. A warehouse reduces errors. A hospital improves scheduling. A small manufacturer installs more precise equipment. A software company automates customer support. A farm uses better sensors. Individually, each improvement seems minor. Across millions of organizations, they raise national productivity and income.

Lesson five: resilience belongs to prepared optimists

The useful form of optimism is not blind confidence. It is the belief that problems can be solved, combined with enough preparation to survive while solutions are being built.

Prepared optimists hold emergency savings, avoid excessive leverage, develop transferable skills, maintain customer relationships, and continue searching for opportunity. They acknowledge recessions, policy mistakes, market crashes, and technological disruption without assuming those events permanently end economic progress.

That mindset captures the central experience of the American economy. Progress is rarely smooth, evenly shared, or politely scheduled. It arrives through experimentation, failure, investment, argument, reinvention, and occasionally a founder explaining that the company is not losing moneyit is merely “pre-profitable.”

Conclusion: Respect the Risks, but Do Not Ignore the Engine

The U.S. economy faces substantial challenges. Federal debt is rising, housing is unaffordable for many families, household borrowing is large, trade policy is uncertain, and technological change may disrupt careers faster than institutions can respond.

Those weaknesses deserve serious attention. They do not erase the country’s structural advantages: a huge internal market, entrepreneurial depth, adaptable labor, abundant capital, strong universities, vast research spending, energy resources, and a demonstrated capacity to commercialize new technology.

The smartest position is not unconditional enthusiasm. It is disciplined respect. Expect volatility. Prepare for setbacks. Question fashionable narratives. Then remember that betting against the U.S. economy has historically required excellent timingand a remarkably high tolerance for being early, wrong, or both.

Underestimate the American economic engine at your own risk. It sputters, overheats, makes alarming noises, and occasionally requires major repairs. Somehow, it also keeps finding another gear.