Beauty Unlocked

Coasting to Retirement with a Margin of Safety

Jul

Retirement planning has a reputation for being about sacrifice: skip the latte, pack sad desk lunches, and somehow become emotionally attached to a spreadsheet with 47 tabs. But there is another approach that can feel more humane: coasting to retirement.

Often called Coast FIRE, this strategy means you have already invested enough that, if you leave the money alone, compound growth could carry it to your retirement target by your desired retirement age. You may still work, but the pressure to save every spare dollar can ease. Your investments are no longer tiny seedlings begging for daily attention. They are closer to sturdy trees that mostly need time, sunlight, and the occasional checkup.

That sounds wonderful. It can be wonderful. But it only works well when you build in a margin of safety.

A margin of safety is the financial equivalent of bringing an umbrella even when the weather app says “partly cloudy.” It accounts for market declines, job changes, inflation, health care expenses, taxes, lower-than-expected returns, and the inconvenient possibility that retirement costs more than binge-watching documentaries in sweatpants.

What Does It Mean to Coast to Retirement?

Coasting to retirement does not mean you are retired today. It means your existing retirement investments may be sufficient to grow into the amount you need later, even if you stop making major new contributions.

For example, imagine Maya is 35 and hopes to retire at 65. She estimates that her household will need about $60,000 per year in today’s dollars during retirement. After estimating future Social Security income, she expects her investment portfolio will need to provide roughly $35,000 per year.

Using a cautious 3.5% portfolio withdrawal assumption, Maya would need around $1 million in today’s dollars to support that annual gap. If she already has $300,000 invested and earns a hypothetical 4% annual return after inflation for 30 years, that portfolio could grow to roughly $973,000 without additional contributions. That gets her close, but “close” and “comfortable” are not always the same thing when the market decides to act like a caffeinated squirrel.

The basic Coast FIRE question is not simply, “Can my money grow?” It is, “Can my money grow enough even if life is less cooperative than my calculator?”

Why a Margin of Safety Matters in Retirement Planning

A retirement plan built on perfect assumptions is not really a plan. It is a motivational poster wearing a blazer.

Markets do not rise in a neat straight line. Inflation does not RSVP before raising your grocery bill. Health insurance premiums do not politely ask whether this is a convenient month. A margin of safety makes your plan more durable when those unavoidable surprises arrive.

1. Investment Returns Are Never Guaranteed

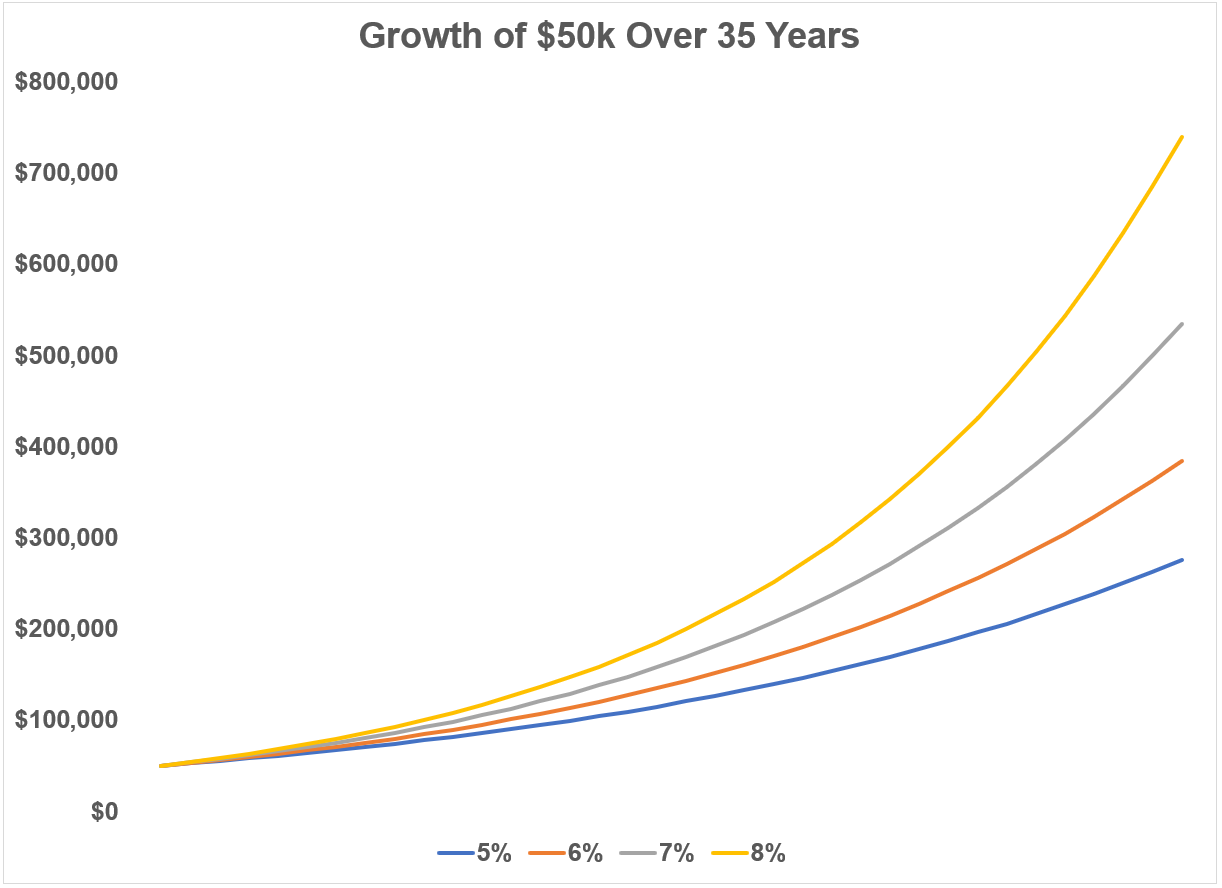

Long-term investing benefits from compound growth, but historical returns are not a promise. A diversified portfolio may experience strong years, weak years, and years that make you want to stop opening your brokerage app until further notice.

For a Coast FIRE plan, it is wise to test several return assumptions instead of relying on one optimistic number. A plan that works at a 7% return but collapses at 4% is fragile. A plan that still works at 3% to 4% real growth has more structural strength.

Think of your retirement target as a bridge. A high-return assumption may make the bridge shorter, but a lower-return assumption makes the bridge sturdier.

2. Inflation Quietly Eats Purchasing Power

Inflation is one of retirement planning’s least exciting villains because it rarely shows up with dramatic music. Instead, it quietly makes everyday life more expensive over time.

Your retirement goal should be expressed in today’s purchasing power, not merely as a giant future dollar number. A $1 million portfolio may sound impressive, but what matters is how many years of housing, food, transportation, travel, insurance, and health care that money can actually buy.

A practical margin of safety includes assuming that some costs may rise faster than your overall budget. Health care, property taxes, insurance, and home maintenance can have their own personalities, and none of them are known for being shy.

3. Sequence-of-Returns Risk Can Change the Outcome

Sequence-of-returns risk is a fancy phrase for a very simple problem: poor market returns early in retirement can do more damage than poor returns later.

If you are withdrawing money during a market decline, you may sell investments when prices are down. That leaves fewer shares available to recover when the market rebounds. It is like eating your seed potatoes during winter and then being surprised when spring becomes awkward.

Even if you are still working while coasting, sequence risk matters because it may affect the final years before retirement. A serious market drop at age 63 is very different from one at age 33 because your portfolio has less time to recover before you begin drawing income.

How to Calculate Your Coast Retirement Number

Your Coast FIRE number is the amount you need invested today so that future growth can meet your retirement target without requiring large additional contributions.

There are several steps involved.

Step 1: Estimate Future Retirement Spending

Start with your expected annual expenses in retirement. Do not automatically assume you will need a fixed percentage of your current income. Instead, consider your actual lifestyle.

- Will your mortgage be paid off?

- Will you downsize, relocate, or remain in your current home?

- Will travel, hobbies, dining out, or family support be important?

- Will you have car payments, student loans, or other recurring debt?

- Will you be supporting adult children, aging parents, or a very spoiled golden retriever?

Many people spend more during the early, active years of retirement and less later. Others spend less at first and then face higher medical or caregiving costs. Your plan should reflect your likely life, not a generic retirement cartoon featuring a couple on a beach holding matching fishing poles.

Step 2: Estimate Reliable Income Sources

Next, estimate future income from sources such as Social Security, pensions, annuities, rental income, or part-time work. Social Security benefits can begin as early as age 62 for eligible workers, while delaying benefits past full retirement age can increase the monthly amount until age 70.

Use your personal Social Security estimate rather than relying on national averages. Your work history, earnings record, marital status, and claiming strategy can all affect the result.

Step 3: Find the Portfolio Income Gap

Subtract reliable retirement income from expected retirement spending.

Example:

- Expected annual retirement spending: $70,000

- Estimated Social Security and pension income: $30,000

- Annual portfolio income needed: $40,000

In this example, the investment portfolio needs to cover a $40,000 annual gap.

Step 4: Apply a Conservative Withdrawal Rate

A common rule of thumb has been the 4% withdrawal rate. However, current retirement-income research often suggests that a lower starting withdrawal rate may provide a larger cushion, especially for people planning for a long retirement and inflation-adjusted spending.

For a conservative Coast FIRE plan, many people test withdrawal rates between 3% and 3.5%.

If you need $40,000 per year from investments:

- At a 4% withdrawal rate, you would target about $1 million.

- At a 3.5% withdrawal rate, you would target about $1.14 million.

- At a 3% withdrawal rate, you would target about $1.33 million.

The lower the withdrawal rate, the larger the margin of safety. You are essentially asking your portfolio to do less heavy lifting each year.

Step 5: Discount That Goal Back to Today

Once you have a retirement target, estimate how much you need invested now for compound growth to reach it by retirement.

This calculation depends on:

- Your current age

- Your target retirement age

- Your current investment balance

- Your assumed annual return after inflation

- Whether you plan to make any future contributions

A retirement calculator can help, but do not let one colorful chart make your life decisions for you. Run multiple scenarios. Try lower returns, higher expenses, delayed retirement, higher health care costs, and a few years with reduced income.

Five Ways to Build a Bigger Margin of Safety

1. Use Conservative Return Assumptions

Optimism is useful for finishing a marathon. It is less useful when projecting investment returns for three decades.

Instead of assuming your portfolio will earn spectacular returns every year, use a moderate real return assumption after inflation and investment costs. You can always be pleasantly surprised later. Retirement planning works better when the good news is extra rather than essential.

2. Keep Contributing Even After You Reach Coast FIRE

Reaching your coast number does not require you to stop saving. It simply gives you more options.

You might continue contributing enough to capture an employer 401(k) match, fund an IRA, build a taxable brokerage account, or invest in a health savings account if you are eligible. The 2026 employee contribution limit for many 401(k) plans is $24,500, while the annual IRA contribution limit is $7,500 for eligible savers, subject to income and plan rules.

Additional savings can shorten your timeline, increase your future spending flexibility, or protect you if returns disappoint. In other words, once you reach Coast FIRE, extra savings become less like homework and more like optional armor.

3. Build a Separate Emergency Fund

Your retirement portfolio should not be your first responder for a broken transmission, a medical deductible, or a job loss. Maintain liquid emergency savings for unplanned expenses.

A working household may aim for several months of essential expenses, while someone approaching retirement may prefer a larger cash cushion. The right amount depends on job security, household income, insurance coverage, dependents, and how flexible your spending can be.

The goal is simple: avoid selling long-term investments during a bad market because your water heater chose violence.

4. Reduce High-Interest Debt

High-interest credit card debt can quietly sabotage a retirement plan. Paying 20% or more in interest is like trying to fill a bathtub while the drain is wide open and somebody has also brought a leaf blower.

Before declaring yourself financially independent, prioritize expensive debt and make sure your monthly obligations are manageable. A lower fixed-cost lifestyle makes coasting easier because you need less income today and less spending later.

5. Plan for Health Care Before Medicare

Retiring before age 65 can create a health insurance gap because Medicare eligibility generally begins at 65 for most people. Private coverage, marketplace plans, COBRA continuation coverage, employer retiree benefits, and a working spouse’s health plan may all play a role.

Health care deserves its own retirement line item. Fidelity’s 2025 estimate suggested that a typical 65-year-old individual could need substantial after-tax savings for health care expenses over retirement, and that estimate did not include most long-term care costs.

A strong margin of safety includes premiums, deductibles, prescriptions, dental care, vision care, hearing care, and the possibility that you may need assistance later in life.

Portfolio Design for a Coast FIRE Plan

A Coast FIRE portfolio should support long-term growth without making you panic every time the market sneezes.

Diversification matters because it spreads risk across different investments rather than placing your future on one company, one industry, or one very confident cousin’s cryptocurrency theory.

Many long-term investors use a mix of broad stock funds, bond funds, cash reserves, and possibly target-date funds. The appropriate allocation depends on your timeline, risk tolerance, pension income, spending needs, and ability to stay invested during downturns.

Target-date funds can be useful because they automatically rebalance and generally become more conservative as retirement approaches. However, they are not magic retirement burritos. Different funds with the same target year can have very different investment strategies, fees, stock exposure, and glide paths.

Your asset allocation should be something you understand well enough to hold through both celebrations and headlines that make everyone suddenly an economist.

Flexible Work Is a Powerful Retirement Safety Net

One of the best parts of coasting to retirement is that it can create career freedom before traditional retirement age.

You may choose to:

- Move from a high-stress job to a lower-pressure role.

- Work part-time or seasonally.

- Start a small business with lower financial risk.

- Take breaks between jobs.

- Negotiate fewer hours or remote work.

- Shift into consulting, freelancing, teaching, or creative work.

Even modest earned income can dramatically reduce pressure on your portfolio. Earning enough to cover groceries, insurance, or travel may allow investments to keep growing longer.

This is why Coast FIRE is often less about quitting work and more about changing your relationship with work. You are no longer asking every paycheck to rescue your future. You are asking it to support your present.

Common Mistakes When Coasting to Retirement

Assuming Your Expenses Will Stay Perfectly Flat

Life costs change. Homes need repairs. Cars age. Parents need care. Children may return home with laundry, houseplants, and emotional complexity. Build flexibility into your plan.

Ignoring Taxes

Traditional 401(k) and IRA withdrawals are generally taxable. Roth withdrawals may be tax-free if qualification rules are met. Taxable brokerage accounts, Social Security benefits, pensions, and side income can also affect your tax picture.

Your retirement income target should be based on after-tax spending needs, not just pre-tax account balances.

Forgetting About Insurance

Health insurance, disability insurance, life insurance, homeowners insurance, auto insurance, and umbrella coverage can protect a Coast FIRE plan from serious disruption. The exact coverage you need depends on your household, assets, dependents, work situation, and risk exposure.

Treating Coast FIRE as an Excuse to Stop Paying Attention

Coasting is not autopilot. Review your plan at least once a year and after major life changes such as marriage, divorce, a new child, job loss, inheritance, relocation, illness, or a major market swing.

Conclusion: Coast With Confidence, Not Blind Faith

Coasting to retirement with a margin of safety can be one of the most liberating financial strategies available. It allows you to recognize that financial independence is not always a finish line. Sometimes it is a gradual reduction in pressure.

The goal is not to predict every market return, medical bill, or future grocery price with supernatural precision. The goal is to create a plan sturdy enough to survive imperfect conditions.

Use conservative assumptions. Build a cash reserve. Invest broadly. Protect against high-interest debt. Estimate health care costs honestly. Consider taxes. Keep flexible work options available. Review your retirement plan regularly.

When your coast retirement plan includes a meaningful margin of safety, you gain something more valuable than a number on a spreadsheet: the ability to make career and life decisions with less fear.

Experiences: What Coasting to Retirement Feels Like in Real Life

Coasting to retirement looks different on a spreadsheet than it does on an ordinary Tuesday afternoon. On paper, the idea is simple: you save aggressively for years, build a strong retirement nest egg, and eventually reach a point where your investments may grow enough without constant new contributions. In real life, though, coasting is usually less dramatic than people expect.

There is no confetti cannon. Your bank may not send a marching band. Most people reach a Coast FIRE milestone quietly, perhaps while reviewing a retirement calculator after dinner or updating a budgeting app between episodes of a show they are only half watching.

The first feeling is often relief. Someone who spent years funneling every bonus, tax refund, side-hustle payment, and suspiciously large birthday check into investments may finally realize that they do not have to live like a monk forever. They can reduce overtime, take a vacation without calculating the opportunity cost of every airport sandwich, or choose a job because it is interesting rather than because it offers the largest possible paycheck.

But the relief can be followed by uncertainty. When you are used to maximizing savings, easing off can feel strange. You may wonder whether you are becoming lazy, irresponsible, or dangerously attached to brunch. That is where a margin of safety becomes emotionally useful, not just mathematically useful.

A well-built safety margin gives you permission to make decisions based on your values. Perhaps you switch from a demanding corporate job to a nonprofit role. Maybe you leave a long commute behind and work remotely. You may decide to become a consultant, work four days a week, or take a lower-paying position that gives you more time with family.

For many people, Coast FIRE becomes a career-reset tool. Instead of saying, “I need to work at maximum speed until age 65,” they can say, “I need enough income to cover my current life, protect my insurance coverage, and avoid touching investments too early.” That is a much more flexible question.

There are also practical lessons. People who coast successfully tend to keep their lifestyle from expanding too quickly. They may increase spending in ways that genuinely improve life, such as better housing, meaningful travel, healthier food, or time-saving services. But they avoid turning every raise into permanent monthly obligations.

That distinction matters. A new hobby is manageable. A giant mortgage, luxury car payment, private-school tuition commitment, and subscription collection large enough to require its own accounting department can make coasting much harder.

Another common experience is learning to tolerate market volatility. Even with a solid plan, watching a portfolio decline during a market downturn can make anyone question whether coasting was a terrible idea invented by spreadsheet enthusiasts. The key is remembering that a coast plan should not depend on perfect annual returns.

A margin of safety may mean you continue contributing during good years, work longer if you enjoy your job, spend less temporarily during down markets, or maintain part-time income. Flexibility turns a financial plan from a fragile promise into a living system.

Ultimately, coasting to retirement is not about doing nothing. It is about reaching a point where your money has momentum, your choices expand, and your future does not depend on squeezing every last drop from your present. That is a powerful place to be.